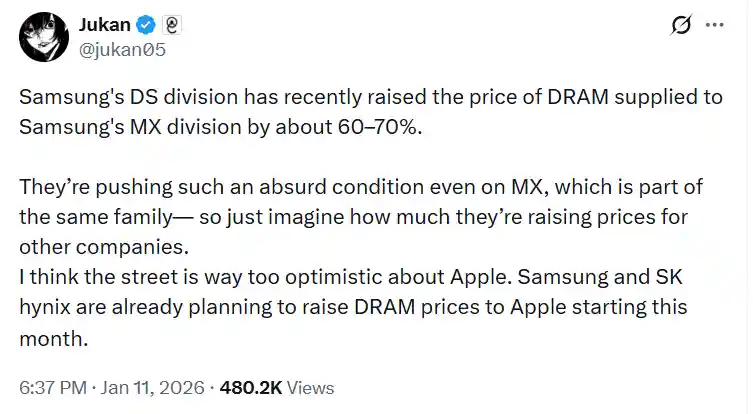

Samsung just did something unusual. Its chip-making arm hiked DRAM prices by 60–70% for its own smartphone division. That’s not how large companies typically operate.

When a business charges its internal teams significantly more for components, it’s making a calculated bet. Samsung believes memory demand is strong enough, and supply tight enough, that even its Galaxy phones will have to absorb the increase. That’s a clear message about market leverage.

The ripple effect matters more than the headline figure. If Samsung is willing to squeeze its own hardware division, external buyers are almost certainly facing steeper premiums. Apple, which relies heavily on Samsung and SK Hynix for DRAM, is already seeing price hikes roll out this month, according to industry sources.

This isn’t a temporary blip. Samsung and SK Hynix control the majority of global DRAM production. When both tighten supply or raise prices in tandem, device manufacturers have limited negotiating power. Apple can’t simply switch suppliers at scale. There aren’t viable alternatives with comparable capacity.

The financial tension is straightforward. Higher memory costs either compress Apple’s margins or get passed to consumers through price adjustments. Neither outcome is particularly appealing, especially in a market where premium smartphones are already testing consumer tolerance.

What’s striking is the confidence behind Samsung’s move. Raising prices internally suggests the company expects sustained demand, likely driven by AI hardware requirements and data center expansion. But it also reveals how concentrated power in the memory market has become.

For investors betting on stable component costs or predictable pricing in consumer electronics, this should prompt a reassessment. DRAM isn’t a footnote expense. It’s a core cost driver. And right now, suppliers hold the upper hand.

Apple will manage. But the broader implication is harder to ignore: memory pricing could tighten faster than the market assumes, and few companies have the leverage to push back.